-

Day 02. 매수 전략Project/BTC_AutoTrade 2022. 8. 25. 22:26728x90반응형

앞 전 포스팅에서 환경설정이 완료 되었다면 이제 실질적인 매수 전략에 대해 알아보자. 아래 포스팅 참고!!

기본적인 매수전략으로 백테스팅 전략을 공부하였다.

관련 코드는 아래 링크 참고하자.

파이썬을 이용한 비트코인 자동매매 (개정판) - WikiDocs

파이썬을 이용한 비트코인 자동매매 (개정판)

이 책은 최근 인기 있는 프로그래밍 언어인 파이썬을 사용하여 국내 3대 거래소(코빗, 빗썸, 업비트) 및 국외 거래소(바이넨스)에서 비트코인을 자동매매하는 프로그램을 개발하 ...

wikidocs.net

파이썬을 이용한 비트코인 자동매매 (개정판) - GitHub

GitHub - sharebook-kr/book-cryptocurrency

Contribute to sharebook-kr/book-cryptocurrency development by creating an account on GitHub.

github.com

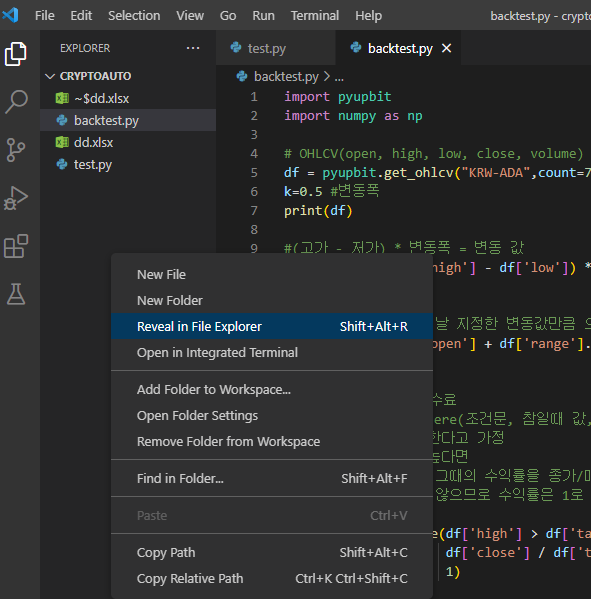

ch07/07_13.py 를 참고하면 다음과 같다.

해당 코드를 vscode 에 복사하여 아래 이미지 화살표버튼을 클릭하면 실행이 되는데

df라는 표를 만들고 해당 df를 dd.xlsx 엑셀파일로 만드는 것을 확인할 수 있다.

해당 excel 파일을 vscode에서 열어볼려면

Shift + Alt + R 또는

다음과 같이 마우스 우클릭 후 Reveal in File Explorer 버튼을 눌러 폴더 위치를 확인하고 엑셀 파일을 확인해 볼 수 있다.

반응형

반응형이제 백테스팅 전략 코드를 해석해보자.

target 이 목표 매수가라고 할 수 있고, 해당 target 으로 매수를 진행했을때의 수익율을 df['ror'] 로 나타낼 수 있고

그 외 누적곱 계산 (수익율을 순서대로 곱해나가면 누적 수익율이라고 할 수 있음), Draw Down 값 (낙폭) , Max Draw Down 값 등을 차례대로 구할 수 있다.

728x90반응형'Project > BTC_AutoTrade' 카테고리의 다른 글

Day 01. 환경 설정 (2) 2022.08.23